Klarna IPO (est. $14.6B) 👀

News from Upstart and Mastercard. Products from Better and Mesa.

Welcome to The Free Toaster! The newsletter for marketing pros at banks and lenders. Inspired by the free toasters banks used to give to each new customer, we’re here to help you acquire more customers at scale. We deliver fresh news, data, and insights to help you acquire more customers—minus the breadcrumbs.

TL;DR

Klarna files massive ($14.6B) U.S. IPO. Upstart announces partnership with DR Bank. Gavin Newsome signs new consumer protection laws in CA. EWA faces potential regulation from CFPB treating it like a traditional loan. Mastercard looks to reinvent checkout with biometrics. Better launches Betsy, a voice-based AI loan assistant. TU’s H2 2024 fraud report reveals a record $3.2 billion in lending fraud. Mesa unveiled their Mesa Homeowners Credit Card.

News

Spotlight of the week:

(11/18) Klarna, the Swedish BNPL giant, filed for a U.S. IPO, hoping to capitalize on the sector's explosive growth, with global BNPL volume soaring from $50 billion in 2019 to $370 billion in 2023. Estimated at $14.6 billion, Klarna’s valuation reflects its U.S. expansion efforts, including partnerships with Apple, Staples, and RiteAid, alongside a push for retail banking services. While Klarna reined in costs with AI-driven efficiencies, analysts debate whether its valuation holds in a competitive market against Affirm, Afterpay, and PayPal. The IPO could be seen as a validation of the BNPL model’s momentum in fintech. [American Banker]

(11/19) Klarna, the AI-powered global payments network and shopping assistant, is teaming up with Google Pay to offer its interest-free payment options starting next year. U.S. shoppers can split payments into manageable installments for purchases above $35, all seamlessly integrated into the Klarna app for tracking deliveries and managing payments. With over 85 million users, Klarna is flexing its muscles as a Buy Now, Pay Later leader, expanding its mission to make flexible payments a checkout norm everywhere. [Klarna]

(11/19) Upstart, an AI-powered lending marketplace, announced a partnership with DR Bank to roll out small-dollar loans for short-term financial needs. The loans, ranging from $250 to $2,500 with APRs under 36%, aim to provide affordable credit alternatives for underserved consumers. DR Bank CEO Jason Hardgrave emphasized leveraging Upstart's AI to expand access to bank-quality credit, aligning with the bank's innovative fintech focus. Upstart’s platform continues to revolutionize lending, helping banks approve more borrowers efficiently and equitably. [Business Wire]

(11/19) Credit card delinquencies have cooled off, with rates declining for the first time since 2021, but the borrowing party seems to be on pause. Despite sky-high interest rates, household debt is growing slower than the economy, and credit card balances per household are still 13% below peak levels. Banks face a tough choice: keep playing it safe or dip into riskier lending to grow their loan books. While consumers have managed thanks to wage growth outpacing inflation, the next wave of borrowing may come when wallets run dry—which could spell trouble if the economy falters. [WSJ]

(11/19) The 2023 FDIC National Survey of Unbanked and Underbanked Households highlights a steady decline in unbanked rates, now at 4.2%, or 5.6 million households, compared to 8.2% in 2011. However, disparities persist, with Black, Hispanic, and disabled households having significantly higher unbanked rates. Lower income and lack of trust in banks remain top barriers. Mobile banking has surged, now the primary method for 48.3% of banked households, while reliance on in-person services has dropped. The report underscores the importance of targeted financial products and education to bridge gaps, particularly for underserved groups reliant on nonbank services like prepaid cards and money orders. [FDIC]

(11/18) California Governor Gavin Newsom signed a slate of consumer protection laws tackling bank fees, medical debt, and subscription traps. Key measures include AB 2017, banning nonsufficient funds fees for instantaneously declined transactions; SB 1075, capping overdraft and NSF fees at $14 or less; and SB 1061, prohibiting medical debt from appearing on credit reports or influencing credit decisions. Meanwhile, AB 2863 requires businesses to provide a "click-to-cancel" option for subscriptions, ensuring cancellations are as easy as signups. These laws aim to ease financial strain on Californians while enhancing transparency and fairness across industries. [Ballard Spahr]

(11/18) Propel Holdings Inc., a fintech innovator providing credit access to underserved consumers, secured a $330 million syndicated credit facility to fuel growth in its CreditFresh line of business. Pathlight Capital joined as a lender, bolstering Propel's efforts to expand its AI-driven lending platform, which has already facilitated over $1 billion in credit. CEO Clive Kinross praised Pathlight's alignment with Propel's mission and growth strategy, highlighting the partnership as a step toward reshaping financial opportunities for underserved borrowers. [FT]

(11/18) Union Credit, after launching its platform one year ago, brought over 20,000 new members to the credit union movement via its embedded lending marketplace. With over 50 credit unions onboard, the platform generated $106M in personal loans, 60% of which went to consumers under 40, while 35% of new members opened checking accounts. By embedding pre-approved offers into platforms like Experian and LendingTree, Union Credit is helping credit unions outmaneuver big banks and fintechs while staying hyperlocal. Its latest tool, "Further," lets local businesses offer instant financing at checkout, driving community spending. With accolades like LendTech of the Year, Union Credit isn’t just reshaping lending—it’s redefining community banking. [Business Wire]

(11/14) The incoming Trump administration could revamp fintech regulations for modern financial tools like Earned Wage Access (EWA), which lets workers access wages early without interest or recourse. EWA, a tool for managing cash flow, faces potential regulation from CFPB rules treating it like a traditional loan, which could impact its availability and push consumers toward predatory alternatives. As fintech innovation democratizes finance, industry leaders call for regulatory frameworks that protect consumers without stifling progress, ensuring tools like EWA remain accessible to underserved communities. [American Banker]

(11/13) The CFPB’s Student Loan Borrower Survey sheds light on the dual impact of student loan debt relief and repayment challenges. A strong 61% of borrowers reported life-enhancing benefits from debt relief, such as pursuing key life goals, while the median recipient received $20,000. However, nearly 42% of borrowers stick to the standard repayment plan, with 31% unaware of more affordable alternatives like income-driven plans. The survey, conducted as the repayment pause ended, highlights the need for better awareness and accessibility to repayment options to ease borrower struggles. [CFPB]

(11/13) TransUnion’s H2 2024 fraud report revealed a record $3.2 billion in lending fraud, with synthetic identities—often crafted using generative AI—driving the surge. Auto lending fraud laps other forms of financing, now accounting for $2 billion of the $3.2B total, and is projected to hit nearly three-quarters of all lending fraud by mid-2025. Auto loans, vulnerable to synthetic identity scams and fraudulent pay stubs, have seen a staggering 105% fraud increase over five years. Meanwhile, shipping fraud spiked globally by 120.7%, highlighting the evolving fraud landscape across industries. [CFO.com]

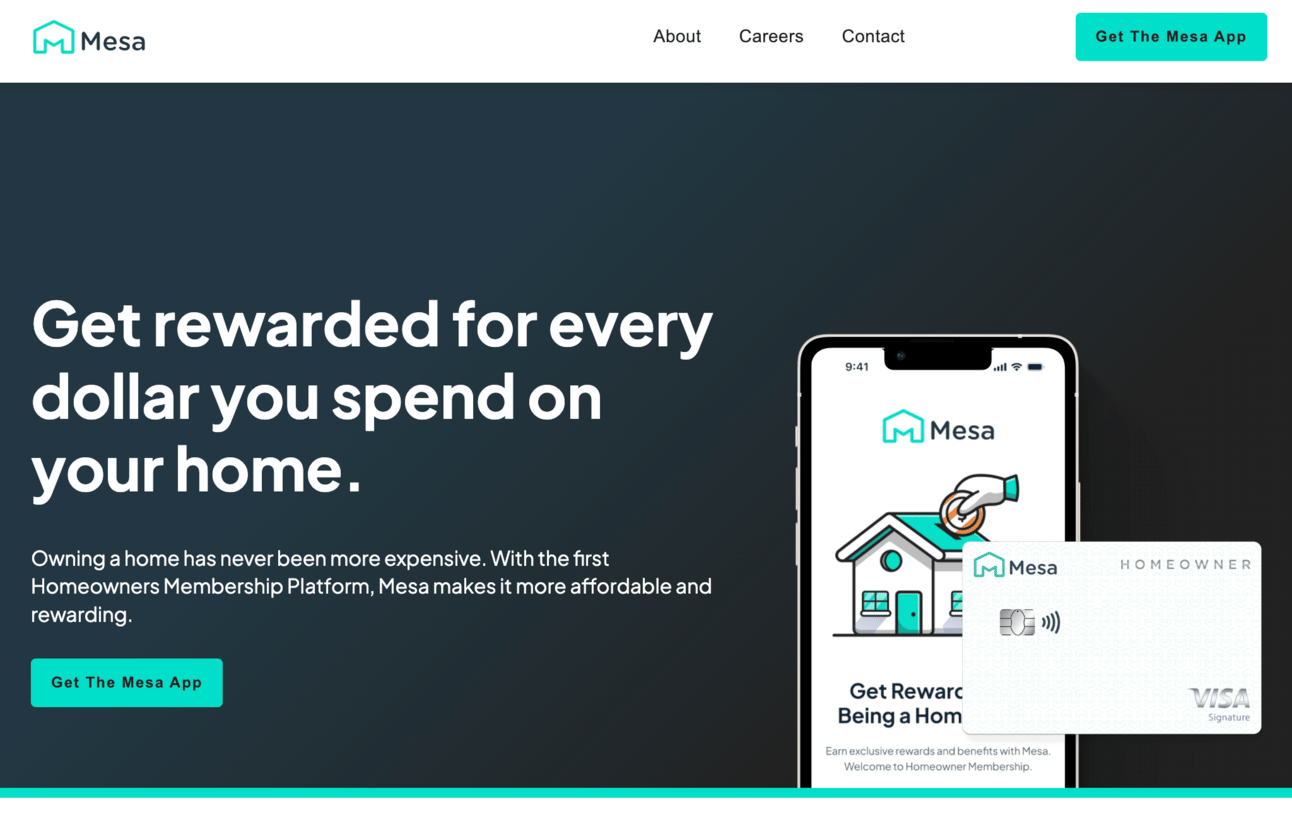

(11/13) Mesa unveiled the Mesa Homeowners Card, the first premium credit card rewarding homeowners for their mortgage payments and home-related expenses. Cardmembers earn 1X points on mortgage payments, 2X on essentials like groceries and gas, and 3X on home-related purchases—all without an annual fee. With over $800 in perks like home improvement credits and big-box memberships, Mesa reimagines premium benefits for homeowners, letting them reinvest points into mortgage payments or other rewards. The card is available via waitlist through the Mesa Membership App. [Business Wire]

(11/13) Mastercard is reimagining checkout with a bold plan to phase out manual card entry and passwords by 2030, replacing them with biometrics like smiles and fingerprints. Using tokenization and secure on-device authentication, Mastercard aims to create a seamless, fraud-resistant shopping experience while introducing numberless physical cards to reduce theft risks. Already, 30% of its transactions globally are tokenized, with programs like Click to Pay and the Payment Passkey Service driving adoption. This transformation promises smoother payments for consumers, higher sales for merchants, and lower fraud for issuers. [Mastercard]

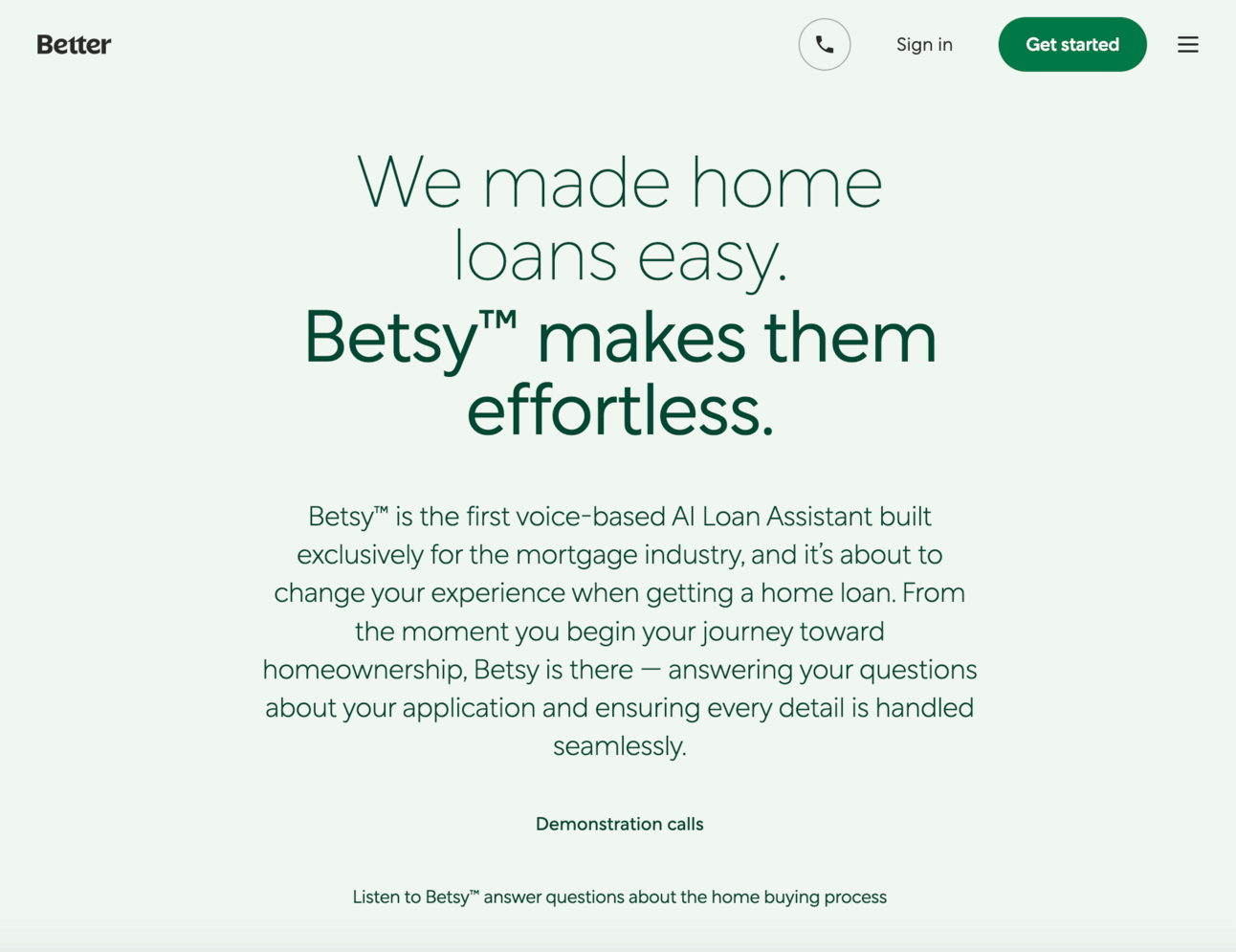

(11/12) Better posted Q3 2024 funded loan volume of $1.035 billion, a 42% year-over-year increase, and launched Betsy, the first voice-based AI loan assistant for the U.S. mortgage industry. Built on Better’s Tinman platform, Betsy enhances customer experiences, boosts efficiency for loan teams, and streamlines the mortgage process from pre-approval to closing. Better continues to diversify its distribution with initiatives like NEO Powered by Better, leveraging Tinman to empower local loan officers and expand reach in the purchase mortgage market, all while focusing on driving profitability through tech efficiency and cost management. [Better]

(11/12) Visa is expanding its Flexible Credential globally, revolutionizing payments by enabling a single card to access multiple funding sources. In the U.S., the Affirm Card now lets users "pay now or pay later" directly through the Affirm app, while UAE's digital bank Liv offers a seamless multi-currency card for frequent travelers. Already a hit in Japan with 3 million Olive cardholders, Visa's Flexible Credential simplifies cross-border payments and boosts financial flexibility for consumers and businesses. This innovation marks a significant leap toward next-generation payment solutions worldwide. [Visa]

Other stuff we’re reading and listening to

Spotlight of the week:

(11/19) CMO Conversations: How Klarna became a fintech super brand (podcast) [WARC]

(11/14) Orrick webinar outlines CFPB rulemaking, GOP deregulation, and rising state enforcement in consumer finance under the Trump administration (webinar) [Orrick]

(11/14) Scott Brown, Group President of Experian, highlights generative AI innovations like the Experian Assistant, an on-demand GenAI tool to accelerate modeling, and Experian Boost, which helps consumers leverage more data to build their credit scores, at Money20/20 USA 2024, emphasizing responsible AI and credit-building solutions (interview) [FinTech Futures]

People

Spotlight of the week:

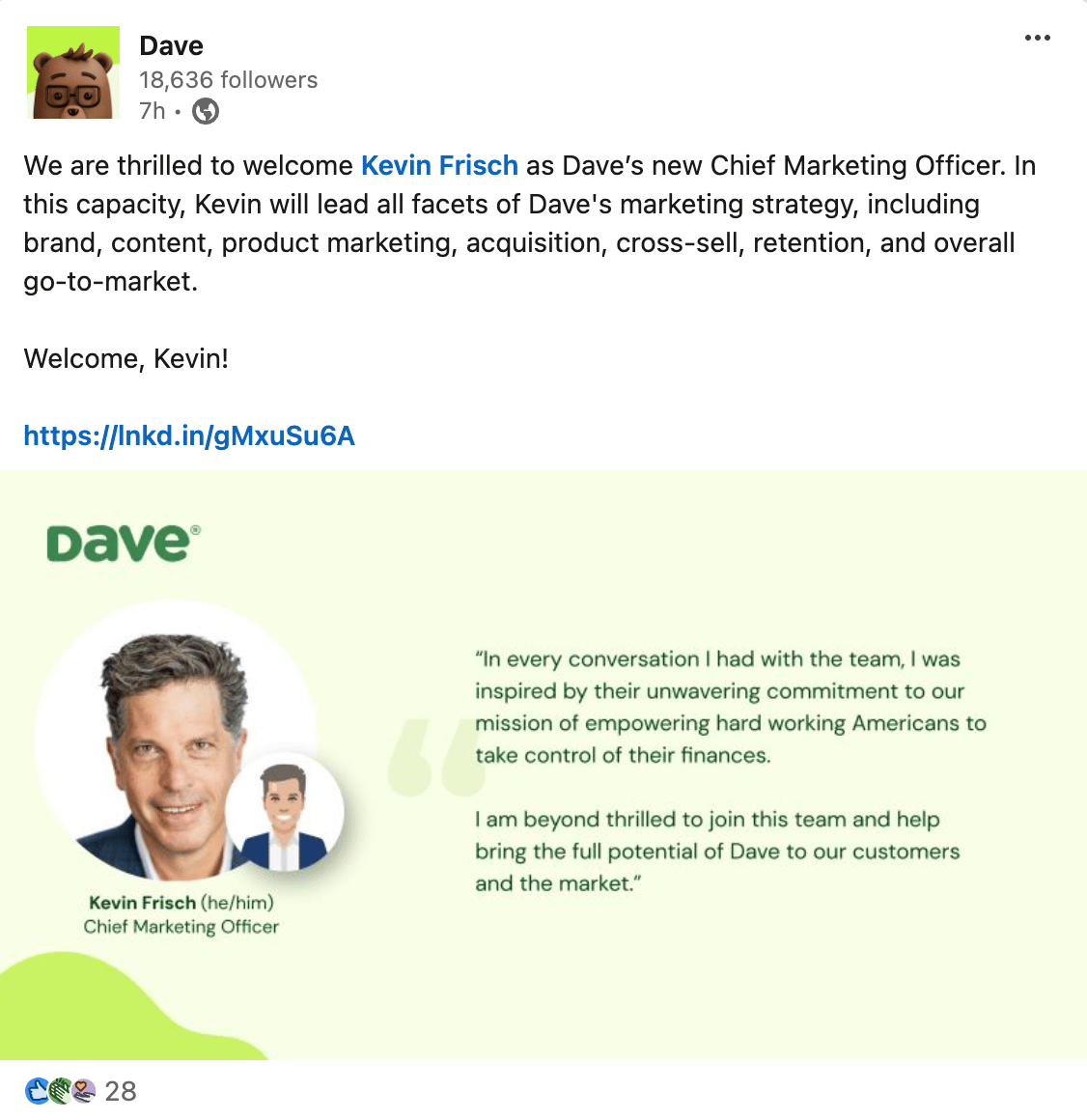

(11/19) Dave, a personal finance app specializing in cash advances and checking accounts, snagged Kevin Frisch as its new marketing chief. Frisch, with a resume that boasts roles at Intuit, Wag!, and Uber, steps in at a crucial moment as Dave faces FTC allegations of misleading advertising about instant cash advances and hidden fees, a controversy they dismiss as "regulatory overreach."

CEO Jason Wilk aims to rebrand Dave from a quick-cash app to a primary banking choice, even as the FTC lawsuit alleges $149 million in controversial “tips” revenue. Frisch has his work cut out, balancing a strategic pivot while building customer trust. [WSJ]

(11/18) Citizens Financial Group appointed three seasoned executives to its Consumer Banking team as part of its transformation push. Raman Muralidharan joins as Head of Mortgage, bringing over 20 years of experience in the mortgage industry, while veterans Adam Boyd and Nuno Dos Santos step up as Heads of Lending and Retail Banking, respectively. The appointments aim to help Citizens grow by leaning into customer-centric innovation. With a solid track record in mortgage servicing, lending strategies, and retail banking, these leaders are set to steer the $219.7 billion institution into its next expansion phase while bolstering its relationship-based banking model. [Business Wire]

Jobs

Spotlight of the week:

Head of Channel Partners at Clutch

Other jobs:

Manager, Demand Generation (Relay)

Director, Channel Partnerships (Trustly)

Head of Growth (Coverflow)

VP of Marketing (Tarro)

VP of Marketing (Gesa Credit Union)

Director of Loyalty, Rewards, and Brand Marketplace (Piñata Rent)

Quick note from our sponsors

NMG and Fiat Growth are excited to sponsor this newsletter, delivering fintech marketers actionable insights and strategies to drive efficient, cost-effective growth. We’re committed to supporting companies as they navigate data-backed decision-making, strategic partnerships, and marketplace success.

NMG helps fintech lenders generate explosive growth on affiliate marketing channels like Credit Karma, Experian, NW, LendingTree, and others.

Fiat Growth is a strategic marketing consultancy dedicated to data-driven decisions, innovation, and execution. We work with leading fintech, insurtech, and rewards brands to build partnerships that scale growth and optimize client KPIs.

Want to build a Newsletter like this? Contact Ghostmode to learn more.